Risk is determined by a number of criteria that affect insurance rates. Drivers may prevent and control expenses by being knowledgeable about these factors. Although premiums vary greatly, your driving history, location, kind of car, and policy level are frequently the key factors. To determine the chance of claims, insurance companies use both statistical data and individual profiles.

Understanding how insurance services function can also offer useful viewpoints, especially when examining how Toyota insurance services are structured in 2025.

Focusing on Toyota Camry insurance rates, which differ based on model features, safety ratings, and repair costs, is made easier by moving from general insurance rates to vehicle-specific charges.

Factors affecting Toyota Camry Insurance rates

Age and Past Driving Experience

Insurance premiums are greatly influenced by a driver’s age, experience, and previous accidents. While a history of no accidents or charges can significantly reduce premiums, younger or inexperienced drivers usually pay higher rates.

Model and Year of Vehicle

The model, year, safety features, and cost of repairs are all taken into account by insurance companies. Modern models with modern safety features could have cheaper insurance. On the other hand, vehicles with expensive replacement components or high-performance models frequently have higher insurance rates.

Regions Risk and Location

Rates can be significantly impacted by where you live. Prices are higher in urban locations with greater traffic and theft rates.

On the other hand, prices may be lower in rural or low-traffic locations. And Weather risks and local regulations also factor into the calculation.

Types of Toyota Camry insurance rates explained

Making educated judgments and analyzing expenses requires an understanding of the many forms of insurance coverage. Each category affects the total premium and has specific purposes. The primary coverage categories for Toyota Camry insurance rates are broken down below.

Liability Coverage

In most states, liability insurance is imposed by law. It pays for any expenses related to injuries or property damage you caused to other people in an accident. There are two primary parts:

Bodily Injury Liability: When you are at fault for an accident and bodily injury, this insurance handles other people’s medical costs and fees.

Property Damage: This pays for damage to another person’s property, such as their car or home..

Collision Coverage

Regardless of who is at fault, collision policy pays for your Camry’s damages in the case of an accident. This is about car crashes with things that are not moving, other cars or road hazards.

Deducted expenses: Expenses that are taken out of your paycheck usually range from $250 to $1,000. Your monthly premiums may go down if you have higher deductibles.

Repair or Replacement: Covers the cost of fixing or replacing your car after an accident.

Impact on rates: Newer Camry models with modern features may cost more to fix, which could lead to higher collision insurance rates.

3. Extensive Protection

Your car is protected from non-collision-related occurrences with comprehensive coverage. Typical incidents consist of:

Criminal activity or theft

Natural calamities or fires

Falling items or creatures

How it affects rates: Comprehensive insurance is usually cheaper than collision coverage, but this depends on the value of the car and the risks in the area.

If you want more help than just regular coverage, it’s helpful to know how Toyota roadside assistance works in 2025, especially when comparing the levels of protection offered.

Policy for drivers who don’t have enough insurance

If you get into an accident with a driver who has this kind of insurance, it will protect you.

not having insurance (uninsured)

doesn’t have enough coverage (underinsured)

It makes sure that your medical bills or car repairs will be paid even if the other driver can’t.

Effect on rates: Raises premiums a little, but gives important protection in places with a lot of risk.

Extra Option of Protections

Some insurance companies offer extra features that could change the total cost of your insurance, such as:

Roadside help: includes getting you back in your car, bringing you gas, fixing flat tires, and getting you to where you need to go.

New Car Replacement: If you total a new car within the first year or two, this policy will pay for the full value of the car.

These insurance policies may cost a little more, but they offer more convenience and protection.

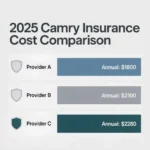

Average insurance rates for a Toyota Camry in 2025

The table below shows an estimated comparison of the yearly insurance costs for a standard Camry model from a number of well-known companies in 2025.

Insurance rates for the Toyota Camry in 2025

You can also read detailed information about Toyota Camry insurance costs, which shows common pricing factors, to get a better idea of how rates change.

| Insurance Provider | Liability Coverage | Collision Coverage | Comprehensive Coverage | Deductible Options | Coverage Limits | Average Annual Rate | Average Monthly Rate |

| Provider A | $800 per year | $400 per month | $300 per month |

$500 / $1,000 per month | $100,000/$300,000 | $1,500 | $125 |

| Provider B | $850 | $420 | $350 | $250 / $500 | $100,000/$300.000 | $1,620 | $135 |

| Provider C | $780 | $450 | $320 | $500 / $1,000 | $50,000/$150,000 | $1,550 | $129 |

| Provider D | $900 | $500 | $400 | $250 / $1,000 | $100,000/$300,000 | $1,800 | $150 |

See https://www.insuranceopedia.com/auto-insurance/toyota-camry-car-insurance for more information. for information, showing the average insurance rates in the US by provider.

6 Expert Tips to Lower the Cost of Your Camry Insurance

To get a lower insurance price, you often need to know how insurance companies figure out risk and how small changes in your behavior or policy could lower your costs. Here are six helpful tips from experts that can help drivers better manage their Toyota Camry insurance rates.

Tip 1: Keep Your Driving Record Clean

A clean driving record is one of the best signs of safety for insurance companies. You can save money on car insurance over time by not speeding, getting into accidents, or breaking the law while driving. Insurance companies look at long-term trends, so driving safely all the time can slowly lower your annual rates.

Why it matters: Insurance costs are reduced when there is less risk.

Tip 2: Modify Your Deductibles Sensibly

Your monthly or annual premium is usually lower if you are paying a greater initial cost. But it’s important to choose a deductible that you can actually pay in the event of an accident. Balancing deductible size and out-of-pocket comfort helps maintain control over your expenses.

Tip: Slightly larger deductibles are frequently advantageous to drivers who usually do not file claims.

Tip 3: Make the most of your annual mileage

Insurance rates are usually lower when you drive less because there is less chance of an accident. If you’ve changed how you drive, like working from home or using public transportation more often, updating your insurance may affect your premium.

How insurance companies see mileage:

Less road time = lower risk = lower cost.

Tip 4: Examine Your Coverage Each Year

Over time, coverage requirements change. You can make sure you’re not paying for protections you don’t currently need by examining your insurance once a year. For example, older Camry models may not need full coverage depending on their current market value.

Points to look for:

Limitations on coverage

Optional extras

The present value of the vehicle

State regulations.

Tip 5: Take Advantage of Discounts

For particular driving behaviors or car characteristics, several insurers provide premium discounts. After qualifying, these discounts are usually given immediately, but you might need to ask for a review.

Typical discount categories consist of:

Programs for safe drivers

Minimal yearly miles

Safety or anti-theft features

Excellent student discounts

Billing without paper

Drivers who want to find more ways to lower their premiums can also look at useful tips that show how small changes can quickly lower an insurance quote.

Tip 6: Get quotes from more than one insurance company and compare them.

Different companies use different methods to figure out risks and set rates, which is why insurance rates vary so much. When you compare quotes, you can be sure that the rate you get is fair based on your needs for coverage and your profile. Major savings possibilities might be found even by examining rates twice a year.

Recommendation:

Use 3–5 trustworthy comparison tools or direct insurer websites to analyze offers.

The most common misconceptions regarding the Cost of toyota Insurance

Misconception 1: Insurance for older autos is always less expensive.

Misconception 2: It costs more to insure a red car.

Misconception 3: Credit scores don’t affect how much insurance costs.

Misconception 4: New drivers don’t need full coverage.

Drivers can make smart choices and avoid spending too much money if they know about common mistakes.

FAQs About Toyota Camry Insurance Rates

Q1: How much does it usually cost to insure a Camry in the US?

A1: The national average is between $1,400 and $1,800 per year, but this number changes from state to state and provider to provider.

Q2: Do the costs of insurance change from year to year?

A2: Older or more expensive cars may cost more to insure, but newer cars often have safety features that can lower rates.

Q3: Will having a clean driving record lower my insurance?

A3: Yes, insurance companies do reward drivers who have little or no claims history.

Q4: Do insurance companies give discounts for having more than one car?

A5: Yes, multi-car policies usually save money.

Q5: Are there tools on the internet that make it easy to compare rates?

A6: Yes, Insure.com and other sites like it offer free comparison tools.

Conclusion

To figure out how much Toyota Camry insurance costs, you need to think about things like your driving history, the details of your car, and the type of coverage you want. Keeping your record clean, looking at different coverage options, and noting any discounts that are available can help you keep your costs down. Checking your insurance from time to time also makes sure it still meets your needs. This helps keep protection that is useful and fair.